.svg)

.png)

.avif)

.avif)

Key Takeaways

Quick Summary: Saving for a home doesn’t have to be overwhelming. With clarity, intention, and the right plan, you can make homeownership feel calm, grounded, and achievable.

- Start with why you want to buy, not just when it’s easier to stay motivated when the goal reflects your values, not pressure.

- Use YNAB to create categories for every part of the process, down payment, moving costs, furniture, and even unexpected expenses, and pad them with a buffer for flexibility.

- Stay consistent by saving early, aligning spending, and working together. YNAB Together keeps couples and families synced so every decision supports the same goal.

We gave this post a category refresh 🗂️ Updated November 12, 2025

We started saving for a house when everything in our life felt settled in the best way.

My husband and I had a sweet little rental from a friend. Our monthly payment was low, the lake was two blocks away, a hiking trail even closer. It was one of those chapters you want to stretch out a little longer, the kind that feels too good to leave.

But slowly, the idea of owning a home together started to take root. Not because it was the “right next step” or because our peers were doing it, but because it began to feel important to us. We wanted a space of our own. A place to settle long-term, stay close to family, and grow our lives together.

We weren’t trying to “upgrade” our life. We were trying to align it. To build something lasting together—not just financially, but emotionally. We didn’t want to feel like we were reacting to life. We wanted to shape it with care.

So we started small. Quietly, intentionally, and with a plan.

We verbalized the new kind of life we pictured and began planting seeds in YNAB. I envisioned a backyard where yellow warblers might stop by on their migration path. We would be those neighbors with just the right amount of garden gnomes and string lights, and who hit Clark Griswold-status during the holidays. My husband would have a cute little three-minute commute, and a grilling area that I would definitely benefit from. Most importantly, it would be ours.

.avif)

Here’s the part I almost hesitate to say: Buying a home and moving? It wasn’t that stressful.

I know moving usually ranks right up there with divorce and job loss. Sure, there were boxes and moments of sticker-shock and a couple of last-minute runs to Target. A lot of Docusign sessions. But we weren’t scrambling. We weren’t overwhelmed. We felt grounded through the entire process. And a big part of that was the YNAB Method of giving every dollar a job.

If buying a home feels far off, or fuzzy, or overwhelming, this story is for you. I haven’t shared our process before. But here it is: how we saved for our home and made the move feel almost... calm.

Step 1: Make Sure Home Ownership is Your Goal

Buying a home is deeply personal. For us, it only started to make sense once we stopped thinking about what we were “supposed” to do and focused on what we actually wanted.

Once we got clear on that, we added “Home Sweet Home 🏠” to our wish farm in YNAB. It wasn’t just a goal anymore; it was a plan. One that felt grounded in what we valued.

Step 2: Get Used to Those Monthly Payments Early

We started setting aside money for a home nearly nine months before we actually bought one. (Honestly? The earlier, the better—just ask Jacob who saved $30k for his down payment in a year.)

At first, it felt a little abstract, like we were funding a “someday” dream. But building it into our YNAB plan made the goal of home ownership feel real. Each time we added money to that category, we were casting a quiet vote for the life we wanted.

One thing that helped us feel extra steady was basing our affordability on just one full-time income. We also didn’t count on side hustles or any income that felt inconsistent. That way, if one of us lost a job, we’d still be able to stay in our home.

That regular rhythm added up. By the time we had an actual mortgage, those payments already felt familiar. We’d made room for them in our spending plan long before the first bill arrived.

Preparedness reduces panic, my friend.

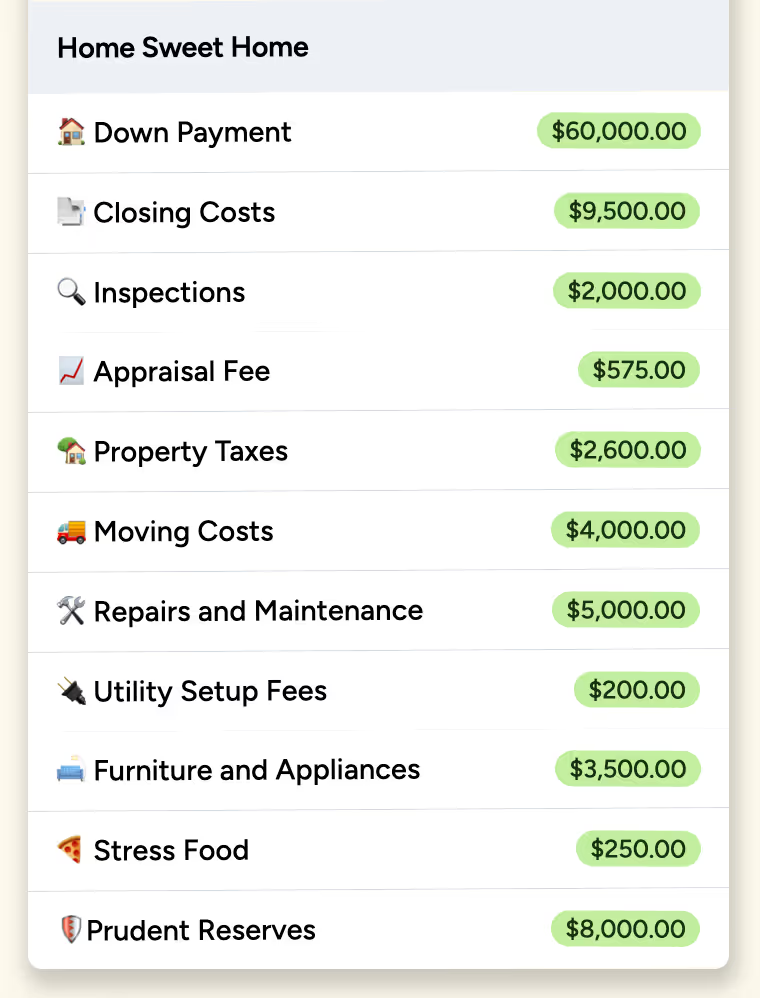

Step 3: Know Your Full Savings Goal

Don’t stop at the down payment when you’re considering how much to save for a home. Zoom out and look at the full (and often sneaky) picture of home ownership. For us, that meant figuring out how much house we could comfortably afford based on our monthly take-home pay, then adding in the usual suspects: closing costs, property taxes, and homeowners insurance.

Then came step two: the less obvious, but no less real, expenses. When we created moving-related categories, we budgeted for the actual transition—movers, utility transfers, a few landscaping updates, new furniture and decor, and Door Dash for the nights when cooking just wasn’t happening. I even added a self-care category for massages, knowing I’d probably throw my back out during the move. (Confirmed.)

Being realistic about the total cost of owning a home will help you feel ready for the full experience—not just the numbers on paper, but the reality of living through it.

If you want help wrapping your arms around a big move, YNAB’s Buying a Home Budget Template is a great starting point. It includes recommended categories and costs that you can easily import and adjust to match your plan.

Step 4: Add a Big Ol’ Buffer

We padded every target in YNAB by about 25 percent for our home purchase and move. That might sound like a lot, but it turned out to be one of the best choices we made.

No matter how detailed your plan is, things will pop up. In our case, my husband got called into work the day before the move, so we had to bring in last-minute help. We tipped our movers more than expected (they were amazing), treated my mom to dinner and a spa day for helping out, ordered takeout three nights in a row when our kitchen was still packed, and added a few "how did we forget that?" items to our Target cart.

That buffer gave us room to roll with it, without the financial stress.

Here are just a few scenarios where a little extra goes a long way:

- You need to hire extra help when your planned helpers (or partner) get called away

- The weather turns, and you need to buy supplies or reschedule movers

- Your new place doesn’t come with curtain rods, trash bins, or a single functioning lightbulb

- A mattress doesn’t fit up the stairs and suddenly you’re renting a truck again

- You eat out more than planned because cooking in chaos is a hard no

- Your inspector informs you that all the “included” appliances are refurbished, and suddenly a home warranty or new appliances feel very worth it

- Moving day turns into an all-hands-on-deck situation, and hiring a babysitter becomes an easy, sanity-saving win

The point is: life happens. A buffer lets you say yes to what you need in the moment without derailing your plan.

Step 5: Shuffle Spending to Increase Momentum

We didn’t overhaul our lives, but we did make space by re-prioritizing our spending. We canceled a few subscriptions we weren’t using, pulled back the reins on dining out, and shifted those dollars into our house fund.

Any extra income—like a tax refund, a small bonus, or birthday money—went straight to our goal. It felt empowering to know those small wins were pushing us forward toward home sweet home.

.avif)

Step 6: Research Loans and Assistance

Comparing loans brought out an inner athlete I didn’t know I had. My husband said it was the most competitive he’d ever seen me, and he wasn’t wrong. I dove deep, comparing four different lenders, and it paid off. That research shaved 0.75% off our interest rate and saved us hundreds in fees.

We looked at conventional loans, FHA loans, and even explored VA and USDA options. (AI wasn’t a thing yet, so we had to do the legwork ourselves—and I’m glad we did. Knowing all the options helped us choose what truly fit.)

We also learned how a larger down payment could help us avoid private mortgage insurance entirely. We kept an eye on our debt-to-income ratio to improve our loan terms and explored first-time buyer assistance programs, just to see what support might be available.

The research took time, but it gave us confidence—and a more stable financial foundation to build on.

And just to say: you don’t have to figure it all out alone. We leaned on the “phone a friend” approach often, asking family and friends who had been through it. Real advice from real people made all the difference.

Step 7: Use YNAB to Stick Together

YNAB Together helped my husband and I stay on the same page, which was a huge stress-reliever in the home buying process. We could both see our numbers in real time, check progress, and make adjustments as we went. No more “Did you use the moving category for fun money?” texts. We were in sync, and that made a huge difference.

We set up a dedicated category for home savings and leaned on spending reports to make sure we were still aligned with our priorities. The loan calculator came in handy too, especially when we wanted to preview different monthly mortgage scenarios and understand how they would fit into our plan.

Remember: with YNAB Together, you can add a loved one—or up to five—to your shared plan at no extra cost. Whether it's a partner, a parent, a roommate, or a trusted accountability buddy, everyone sees the same plan and can work from the same numbers. That kind of transparency makes it so much easier to move forward with confidence, together.

Where Attention Goes, Energy Flows

There’s a saying I love from yoga: where attention goes, energy flows. That’s what saving for a house felt like for us. Every time we added to that category, we were quietly affirming that this mattered. And over time, that steady focus built real momentum.

By the time we got the keys, it didn’t feel like some giant leap. It felt like the next step in a journey we’d been walking toward for a while—one decision, one dollar, one conversation at a time.

Want to make sure your money reflects your new reality? Here are 20 questions to ask yourself after a move.

Saving for a house isn’t just about hitting a number. It’s about clarity. It’s about figuring out what you actually want, and then building a plan that reflects it.

YNAB helped us turn a big, slightly overwhelming goal into something specific, doable, and personal. It helped us move with intention.

If home ownership is part of the future you want, whether individually or with a partner, you don’t have to figure it all out today. Start where you are. Create the category. Fund it when you can. Let your attention shape your direction.

You might be surprised how quickly the pieces come together.

Try YNAB for a free month and discover the stress-reducing magic of having a plan that fits your life.

.png)

YNAB IRL: “We saved for a down payment for a house in a couple months and had perfect clarity the whole time!”

Meet Kamila, who funded a house, international move, and baby with picture-perfect clarity.

%20(1)%20(1).avif)

We decided to buy a house and casually started setting money aside for the down payment. We saved around €15,000 in a couple months (we actually started saving right after our wedding which was also a big splurge and we paid for all of it in cash). Then we decided to speed it up and actually found a beautiful house that we wanted (it was only a project at the time, waiting to be built).

After that, the construction started and they offered us to make changes to the planned house, which we had to pay for (like every additional electrical socket, better lighting, bigger bathtub, better hardwood floors, you get the idea...).

So right after we triumphantly knocked the down payment out of the park, we immediately had to start saving again for all these extra wishes. In a year or so, we saved another €60,000, even though I got pregnant along the way. This not only meant a decrease in income, but also setting aside a couple thousand to prepare for the baby and to buy all the necessary equipment.

Having YNAB through the whole journey made everything possible. We always knew how much precisely we could afford to throw in the house categories, so that we still had enough for our bills, true expenses and daily lives. We had perfect clarity from day one. We asked ourselves on multiple occasions, how do other people do it without YNAB? How do you decide whether you can afford to pay 50k down payment, when you don't know what your money is supposed to be doing?

I couldn't be more grateful that we found YNAB and that we use it every day. It changed our lives!

.avif)