.svg)

.png)

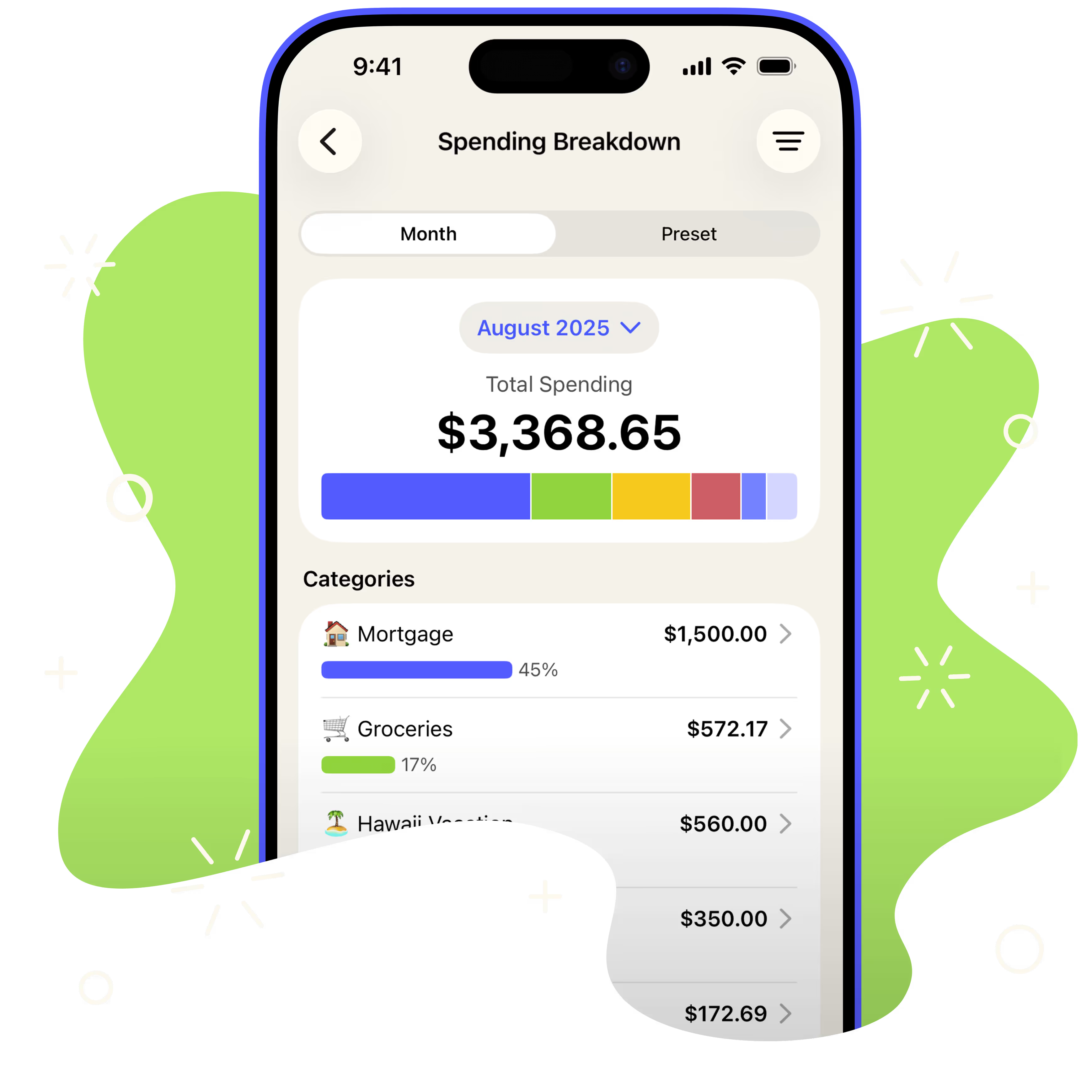

By spending intentionally, you’ll know where your money goes...

and where it can take you.

App Feature

Goal Tracking

Get good with money and fund a future you’ll love to live.

.avif)

Clarify your goals

Getting clear about your priorities and goals makes it easier to create a plan for your money that will add more value to your spending—and your life.

Plan your spending

Eliminate guilt or second-guessing by knowing what you want your money to do for you. Intentional spending is easy when you give every dollar a job.

Visualize your progress

Being able to see how much you have and how much you need to reach your goals at a glance helps build more momentum. We’ll even do the math for you!

93%

of YNAB users say they can confidently cover a $1,000 emergency

Based on the average of 2025 survey responses

Simplify saving

Targets help you have what you need and get what you want. Decide how much money you want to spend and YNAB will calculate how much you need to save each week, month, year, or by a custom date to reach your goal.

.avif)

Stay focused on the future

Get helpful reminders of how much money you need to add to a category to stay on track and watch as you get closer to achieving your goals with color-coded progress bars.

.avif)

Save at your own pace

If something comes up, you can choose to snooze your target for the month—life happens, so change your plan without guilt or stress. Just pick up where you left off next month.

.avif)

Build healthy (helpful) habits

Intentional spending leads to effortless saving—as you spend less, you save more. As you start to consistently reach your goals, you’ll begin to see your money as a possibility instead of a problem. Live a life free of money worry.

.avif)

Get good with money

Make your money meaningful

.avif)

Live a well-spent life.

Stop worrying about money (for good!) by creating an intentional plan that reflects your priorities and supports your dreams.