.svg)

.png)

.avif)

If you’re just arriving on the post, make sure you read the comments, where some of my assumptions are generously corrected.

On Friday I said I’d be evaluating all my major expenses, and decide whether to:

- Downsize my house

- Have no more children

- Take my kids out of private school

- Become a one-car family

- Drop or reduce my health insurance

- Drastically reduce grocery spending

As I started to research whether downsizing the house is a good idea, it occurred to me I’ve never established a long term financial goal, like, you know, retirement. Deciding whether to make major changes to my big expenses is only meaningful in terms of the impact on my long term goal – so that’s where I need to start.

Shocker: I Want to Be Debt Free with a Nice Nest Egg

My major goals are similar to yours:

- Eliminate all debt (including home mortgage) by the time I’m 50 (16 years from now).

- Draw $40,000 per year from my investments starting at age 54 (20 years from now).

Barring catastrophe, the debt elimination goal is on track. I’m already rolling a pretty good debt snowball, and as long as I don’t interrupt it, my home loan will be zero right around my 50th birthday.

By the way, if you have debt, and you’re not snowballing it, you need to start. The day you start snowballing – however modestly – your feelings about your debt will change. You’ll still feel annoyed and stressed by the balances, but you’ll shift immediately toward a sense of control and power. And…

Debt snowballing is addictive.

My current plan zeroes all debt in 16 years, but the momentum of a good snowball could easily knock that down by 3 to 5. Why? Because the more the snowball grows, the more excited you get about eliminating balances. The excitement drives more dollars toward the snowball, accelerating it.

If you’re YNABing, it’s all the more fun because every time you have extra money in a category, you can slide it right into your debt repayment. Double the emotional payoff and patting of self on the back.

So, that’s the debt freedom goal. I’m sure there will be ups and downs along the way, but as long as I’m living on a budget and working to improve my earning power, I’m confident the debts will go away on schedule.

I Have to Save How Much if I Want to Retire in 20 Years??

The retirement income, on the other hand, is a can of worms. This is my first real foray into the messy world of investing, inflation, and withdrawal rate in retirement.

Here are the assumptions I’m working with; feel free to jump in and correct any you consider way off base:

“Retirement” Date: 2033 (age 54)

By age 54 I’ll have no debt and no kids at home (right, parents over 55? Please don’t burst my bubble). My son will be 26, daughter 24, and if there are any more Butler kids on the way, he/she/they will be 18 (or close to it).

*I’ll put all their belongings in suitcases and on the front porch, then kick them out at 4am on their 18th birthday. In my head this is a scene played out between Cliff, Theo, and Vanessa Huxtable. I don’t know why.

Retirement Income Goal: $40,000 per year (in 2013 dollars)

Based on our current budget – with no kids and no debt – Kate and I would live fine on $40,000 per year (again, in today’s dollars). Not lavishly, but comfortably.

We may not even need the $40,000 when I’m 54 – I should be in my peak earning years. But assuming I’m completely fed up with all income-generating activities, $40,000 per year would do the job.

Trying to Predict the Stuff You Can’t Really Predict

- Inflation: 3.25% per year (the historical average).

- Number of years in retirement: 40 (assuming I make it to age 94. If I die earlier, the remainder can go to charity – or to build a shrine honoring John Elway’s Super Bowl wins).

- Interest rate earned on investments during retirement: 4.25% (I really had no idea what to use here, and went with the default number on the calculator shown below).

So how big does my nest egg need to be, and how much do I need to be saving to get there?

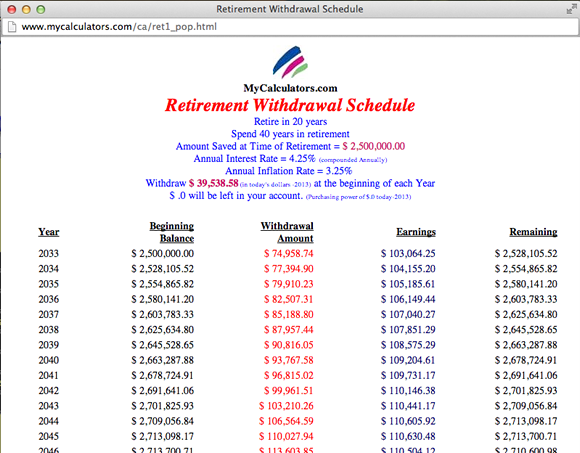

The numbers I need to hit if I want to draw $40,000 per in 2013 dollars, starting in 2033, and lasting for 40 years. Retirement Withdrawal Calculator here.

Plugging my numbers into this calculator, it appears I need to have $2,500,000 earning 4.25% per year, with an average inflation rate of 3.25% per year – and all of that would allow me to start drawing $40,000 in 2013 dollars from age 54 on.

$40,000 per year in inflation-adjusted income, starting in 2033. (Only showing the first 15 years or so.)

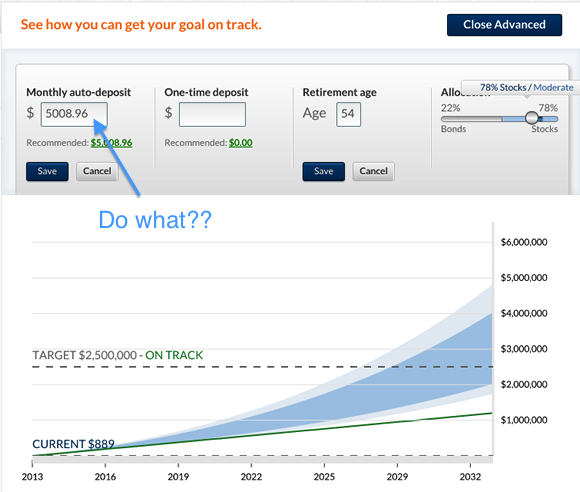

This is Where Things Get a Little Nuts

Betterment gives me about a 75% chance of reaching my savings goal on time…with a monthly deposit of over $5,000 per month??

According to Betterment, if I want to have a (roughly) 75% chance of having $2,500,000 at age 54, I need to be saving around $5,000 per month.

Hm.

If I were making $250,000 per year, $5,000 per month would be reasonable. Unfortunately, I’m not. (It is worth mentioning that improving your earning power – once you’re solidly living on a budget – changes your retirement prospects in a major way.)

That’s One Heck of a Reality Check

So, why did I take you through all those goal calculations, when I’d obviously already found out they were unrealistic?

Because maybe you’re like me. Maybe you think $40,000 is a piddly retirement income – one that I could achieve by beginning to invest when I’m 45 or so. If you do think like me – oh how wrong we both are.

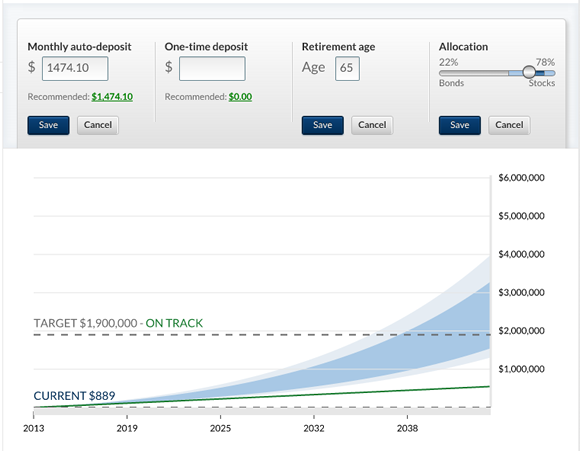

For example, dropping my annual income goal to $25,000 (2013 dollars), and extending my retirement age to 65 (giving me 31 years instead of 20 to prepare), changes my monthly savings requirement to $1,475 – a savings rate I could achieve within the next year or so.

$1,475 per month to reach a $1,900,000 nest egg by age 65. Much more feasible.

Don’t Forget About the $729,000 Bonus I’ll Get at Age 65

Remember how all my debt will be gone when I’m 50? Taking the whole snowball and putting it into my investments for the fifteen years between age 50 and 65 will pad my nest egg with a tidy $729,000, bumping my retirement income from $25,000 to $34,000 per year. It pays to be debt free.

Sheesh – 1,000 words (and one John Elway reference) later, that’s my best guess at a retirement plan.

How’d I do?

.avif)