.svg)

.png)

.avif)

.avif)

.avif)

Key Takeaways

Quick Summary: Paying off debt is great, but staying out of it for good takes a different kind of strategy. Before you attack balances, build a plan to prevent future debt.

- Save monthly for non-monthly expenses like car repairs, holidays, or vet bills so surprise costs don’t push you back into debt.

- Use your budget to plug the leak first, then direct what’s left toward steady debt payoff.

- Once you’re debt-free, get one month ahead to create lasting financial breathing room and real peace of mind.

Fresh as your paycheck on payday 💵 Updated: September 17, 2025

Stuck in the debt cycle? Here’s how to prevent future debt and stay out of debt forever.

You work so hard to pay off every last cent of your debt—and you do it! It’s finally gone! But then time goes by—and in a cruel twist of fate, when it rains it pours. After a one-two punch of unexpected expenses, you find yourself sliding into the hole of debt once again. What could be more frustrating?

We hear this over and over again. What’s going on? Why is it so hard to break the cycle of debt?

Recently, we finished our very first Debt Bootcamp—a multi-week webinar/community/challenge of aggressive debt payoff and 8,000 people joined us. Not only did they collectively pay off $1.5 million in just two months, it was so inspiring to watch them all achieve their goals and support each other.

During this debt bootcamp, I started to see these lightbulb moments for the people that found themselves stuck in the debt cycle. It’s this: what’s the first thing you should do in aggressive debt payoff? Increase your debt payments to tackle credit card balances? No. The first priority is to use that money to prevent future debt.

Of course, if you're familiar with YNAB (You Need A Budget), you realize that's simply saving for non-monthly expenses. This is what helps people prevent future debt—and I saw people just latch onto this idea in the bootcamp for the very first time.

Let me explain it this way…

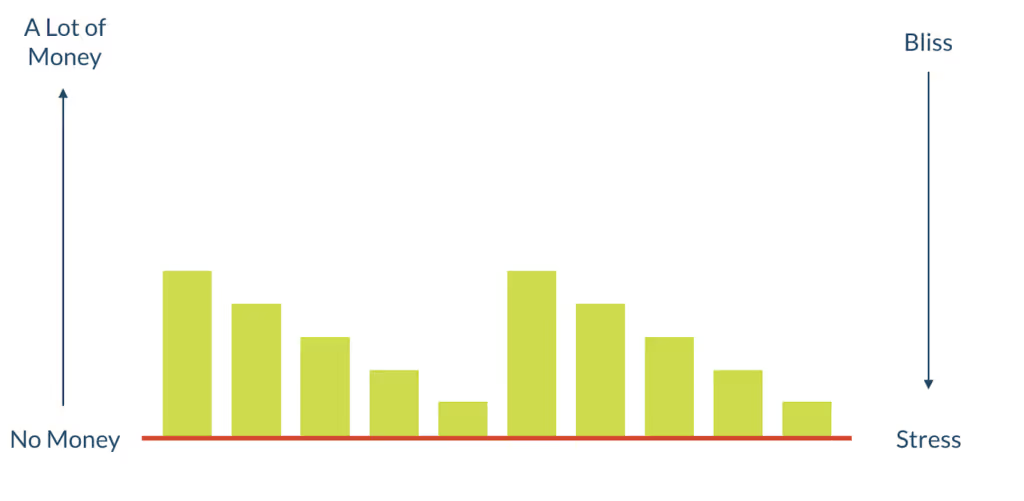

The paycheck to paycheck cycle looks something like this:

Money comes in (green) and our balances go up. Then money goes out, and our balances go down. They go so far down, in fact, that they’re right at the financial edge—zero. Living like this is stressful—you have no options and no flexibility because you have no cushion.

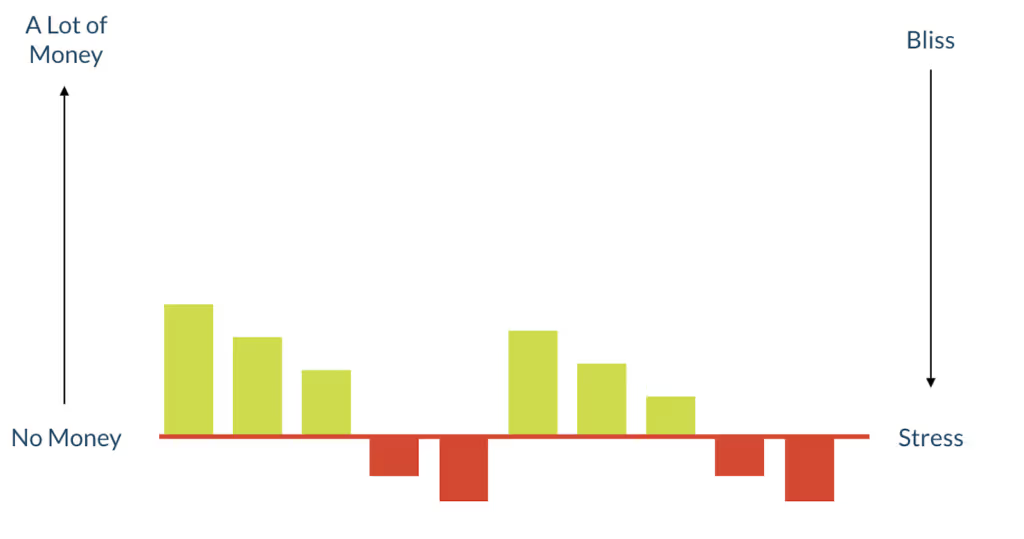

However, many people are living in a spending cycle that’s even more stressful than teetering on that financial edge—and that’s the debt cycle.

In this cycle, money comes in and your bank balance is positive, but you don't quite make it to the next paycheck. You can't quite cover all of your monthly payments and regular budget items, like groceries, along with discretionary spending. Out comes the credit card so you can get by for the rest of the month. You climb back out only to dip back in. When the credit card payment comes due, you end up making minimum payments at a crazy interest rate to stay afloat with your other payments, such as mortgage payments and auto loans.

Typical Debt Repayment

When people are trying to get out of debt, they have a tendency to throw every extra dollar at the debt. This is what we're told to do! “Debt is bad! Get rid of debt! You are bad if you have debt! Debt = bad! You = bad!” Faced with that messaging, you may think the best option is to go all in on getting out of all your debts

Why Attacking Your Debt Aggressively Doesn’t Work

So you do just that: you scrimp, save, and toss every extra dollar at the debt. Some people even take out a debt consolidation loan. And then…the car breaks down. But how do you pay for it? All your extra money went to paying down debt, because wasn’t that what you were supposed to do?

So the car fix goes on the credit card, and then the debt cycle repeats. Pretty soon, you've gotten further and further in consumer debt with high credit card balances, when you were trying to do the exact opposite.

And that's the root problem! Before you can work aggressively on paying off your debt and break free from those nasty interest payments, you need to first break the cycle of debt.

Imagine that I’m in a rowboat on a lake, and I notice that my boat has sprung a leak. What’s my natural instinct? “Oh my gosh there’s water seeping into my boat, I need to get it out!” Yes, you do. But the bailing will be far more effective if you plug the hole first.

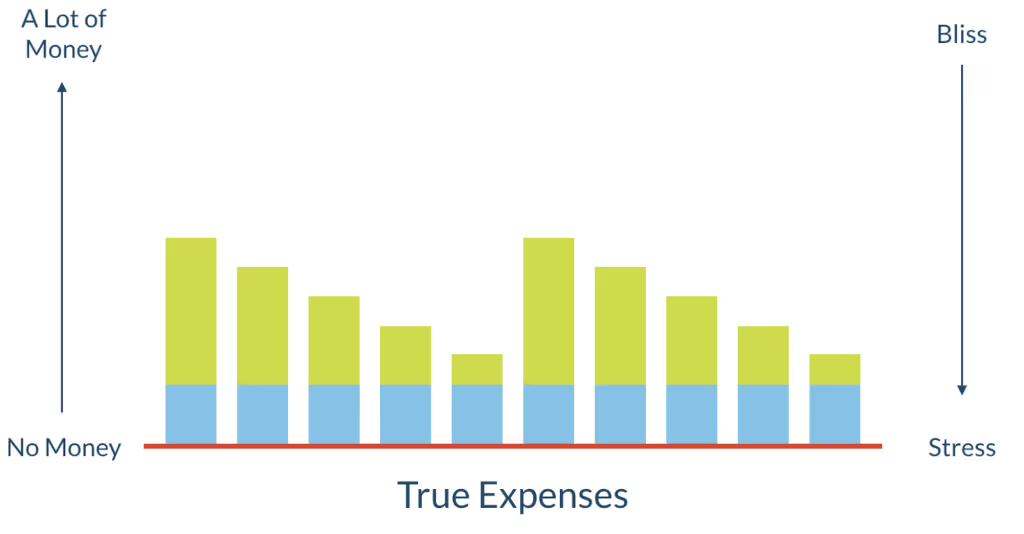

Lucky you, we have a proven method to help you plug that hole—save for your non-monthly expenses (aka true expenses). These are all the things you don’t spend money on every month. Some of them are predictable, like Christmas every December, and some aren’t, like that car repair you had no idea was coming.

You may be thinking, “What in the world do non-monthly expenses have to do with debt?”

Oh my friends. So much. This method is the antidote to debt.

A Proven Method for Debt Prevention

Let’s go back to our example where you’re sending everything you have at the credit card (or whatever debt you’re trying to slay). Let’s say it’s $500 a month.

Instead of sending ALL that money out the door every month, you take a step back. You decide to hang on to:

- Christmas: $50

- Car Repairs: $100

- Vet Bills: $40

- Annual Car Registration: $35

___________________________

- Total: $225 a month

You're still sending $275 dollars to your credit card debt. This is a simplified example, most of us have more non-monthly expenses than this, but you get the idea. You're building a safety net—and weaving it together month by month.

Check out our non-monthly expenses template for a comprehensive list of all the things you don’t spend money on every month!

Three months go by. Your car needs a new tire for inspection. It will cost $150, but you have saved $300 for repairs.

Hurrah! You just prevented debt!

You don’t need that credit card! You’ve also paid off $825 on your credit card ($275*3 months). You’ve made progress without taking a single step back. This is how you break the cycle of debt. As time goes on, you find yourself in this situation:

The spending and earning cycle that we all go through is happening on top of this pile of cash that you saved! Yes, it will ebb and flow: perhaps you needed new tires and the car repair category dipped. The months go on (as you drive on your safe, new grippy tires) and you build that car repair category right back up again. A few months later the cat needs a check-up, but you've got the money, and it won't go on the credit card, taking multiple payments to cover. It's no big deal, and you didn't need to charge it.

Then a day arrives when your debt is gone. You pause to do a little celebratory dance, because it was a lot of work. And now that $275 that was going to pay off debt each month is yours to assign wherever you need or want it—and that feels pretty darn good.

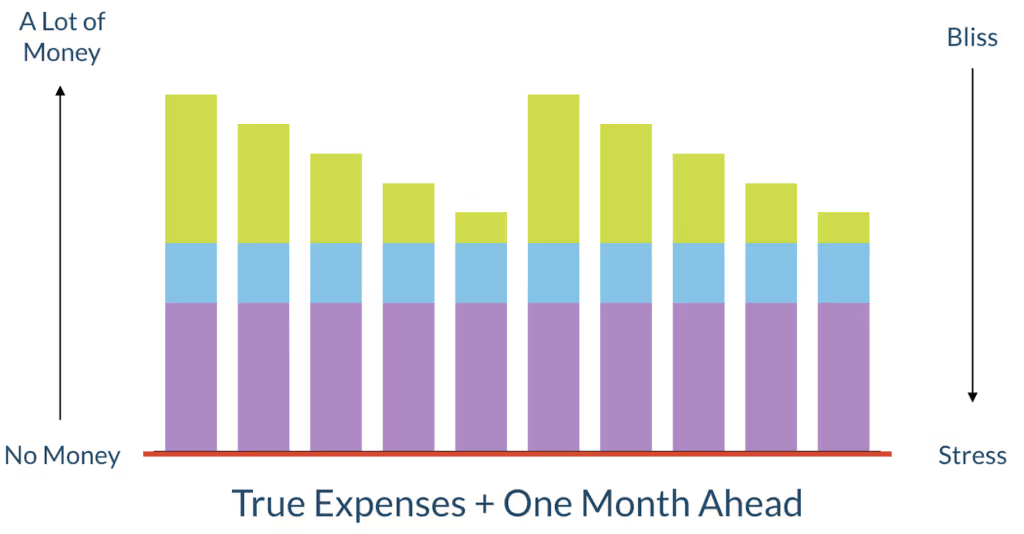

Debt Prevention Nirvana: Getting a Month Ahead

But it gets even better than this if you work on getting a month ahead. When you’re a month ahead, your spending for next month is completely funded before the new month rolls around. I know it sounds impossible, but you'll get there, you really will! It takes most YNABers 4-6 months to get to this point (full disclosure: it took me a year). But once you're a month ahead, it's a glorious thing.

Look how high up that spending and earning cycle is! It's sitting fat and happy on an even bigger pile of cash. It's a long way down to get back into debt, and that's exactly what we want. You've got more money than you need to pay all of your monthly expenses, and plenty more to spare. We want a big distance between you and the financial edge. You're prepared to handle almost anything that life throws your way, from medical bills to a large down payment on a new car (preventing a big car loan) when your old one breaks down.

The Magic of Budgeting For Debt Payoff

This is the magic of budgeting: it helps build a barrier with your dollars that debt can’t get through.

If you've been struggling with the cycle of debt, throwing every penny you have at your balance, take a step back. You can get debt-free, you just need the right strategy. Start saving for those things that are causing you to reach for the card.

Debt prevention is just as important as debt pay down. In fact, it’s the critical first step.

.avif)