.svg)

.png)

.avif)

.avif)

Several years ago, my wife Julie sent me a glorious text:

Julie: “Hey, I’m at Costco. Do you want anything in particular?”

Me: “Well, what do they have?!”

If you’re not clear on what you want, someone will certainly come along and tell you. So it goes with purchasing a home. Before you know it, you’ve committed to the one of the most expensive purchases of your life and you’re not even sure you can afford it.

So how do you know how much house you can afford?

The Problem With Rules of Thumb

If you’ve done any rudimentary Googling on this topic, you’ve doubtless run into many-a-calculator that will happily spit out a maximum house payment amount you could “afford.”

You’ll often see these rules of thumb touted from the Gospel of Absolutes:

“Your mortgage should be no more than 25% of your take-home pay.”

Or to complicate things:

“Your home expenses should be no more than 28% of your gross monthly income.” (Wait, huh?)

Or this one:

“Your total debt payments should be no more than 36 percent of your gross income.”

Rules of thumb only get you so far. And honestly, they tend to give an overly simple answer to a complicated question. And sometimes they contradict each other!

Instead of letting that third, fourth, or fifth home affordability calculator hand you yet another cookie-cutter answer, it might be time you asked yourself some hard questions.

3 Questions You Need to Answer (And Google Won’t Help)

What follows are some questions to get the gears turning. We’re going to try and avoid the Costco situation by proactively determining what you want instead of being told what you want and reacting (emotionally) in the moment. Obviously, if you’re making a home purchase with a partner, do these exercises together. (Even more interesting: Do them separately and then compare notes!)

1. What Are Thirty Must-Haves for Your New Home?

Thirty?! That’s right.

Grab some sticky notes and start writing. Be descriptive. Don’t write “Kitchen.” Write “A kitchen fit for Top Chef. Stainless steel as far as the eye can see.” (Use big post-its.)

If we do only five sticky notes, 95 percent of you would come up with the same list, which isn’t very instructive. We want to work past the easy ones, deal with the moderately-difficult items, and then really claw for those last eight to ten. Don’t do less than thirty.

The last eight to ten is where the magic happens because your imagination starts to run a little wild—your brain starts turning a few gears that hadn’t turned for a while.

Now rank them. The top item is the most important and they become less important as you work your way down. Go quickly. Follow your gut. If you’ve done this with a partner, you’ll be ranking sixty post-its. Cluster similar post-its and rank them.

2. What Are Your Non-Negotiables?

While our question above called on you to come up with “must-haves”, we also forced you to come up with thirty. This is by design. Now that you’ve clearly articulated your must-haves (with vivid, emotion-inducing descriptions!), find the point in your ranked list where the non-negotiables stop.

If you’re working through this exercise with your partner, can you both agree on that point?

We’ve expanded our horizons and reached for the stars with question one, and now we’re moving a bit closer to a—shall we say—more realistic imagined reality. Somewhere in that list, your heart kind of tells you, “Well, it’d be okay to stop here. The treehouse in the backyard isn’t that important.”

Or, on a more serious note, it could be something like, “The kids could share a room. We don’t need that fourth bedroom.”

We’ve come at this from the angle of what you really want from this house. Now, we need to come at it from another angle entirely.

3. What Spending Would We Happily Give Up to Get This House?

Whether you’re a veteran YNABer and know what you’ve spent in every category for the last five years, or you can’t remember what you spent five minutes ago, here’s where we start trying to fit your future home into your situation using…tradeoffs.

Grab those trusty sticky notes again. List every single expense—one-off or recurring—that you would happily give up, or an income source you would seek, in order to purchase this house of sticky notes.

- Would you cut back on any items?

- Trim the budget here or there?

- Would you take less-extravagant vacations?

- Fewer vacations in total?

- Would you eat out less, and eat in more?

- Would holiday spending become a less-expensive affair?

- Would you drive a less-expensive car?

- Become a single-car household?

- Would you…stop contributing to your kids’ college savings?

- Would you reduce your retirement contributions?

- Would you have your significant other get a job now that the kiddos are in school? Or moved out?

- Would you keep grinding away in a job you don’t like just for the “great pay?”

- Would you work overtime?

- Would you get a second job?

Some of my example items, written on imaginary post-its, maybe have rubbed you wrong. Jesse! You wouldn’t stop contributing to your retirement to purchase a home!?

Well, no. But if purchasing a home we can’t reasonably afford would keep me from spending, investing, and saving the way I want to—isn’t that the same thing?

Now Pretend You Bought the House

This step works for determining how much house you can afford, or if you should hire that person to help you with your side gig: Pretend you’ve already done it.

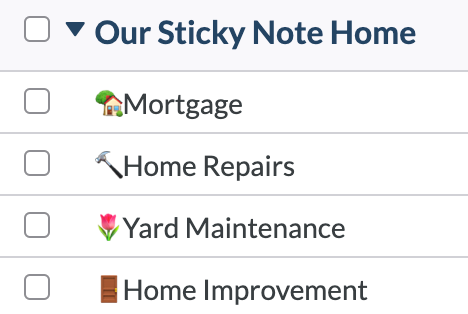

Get into your budget and set up a Category Group called “Our Sticky Note Home.”

Don’t use YNAB yet? You can set up a practice budget totally for free in our 34-day trial, and we won’t even ask for your credit card.

Within “Our Sticky Note Home” Category Group, setup categories for:

- Mortgage payment increase: This category is going to be the difference between what you’re paying now (your rent or if you already have a mortgage) and the monthly payment on the future home (don’t forget to add property taxes, homeowner’s insurance, and perhaps PMI). Here’s an example: if your current Rent/Mortgage is $1200/month and your new mortgage would be $1800/month, this category amount would be $1800-$1200, or $600.

- Home repairs. If you’re already a homeowner, this one’s easy. A good rule of thumb (there’s that cheat again!) is one-half to one percent of your home’s value each year. This may seem like a lot of money, but—roofs.

- Yard maintenance. The mower, edger, leaf blower, shears, bins, garden tools, etc.

- Home improvements. If you don’t think you’ll want to improve things before you’ve even moved in, oh boy are you in for a treat.

Now fund those categories. And next month fund them again. Every time you get a paycheck, you’ll be pretending you already bought the house, already are saving for home repairs, already bought the sweet little battery-powered leaf blower, and have some curtains picked out for improvements.

How’s your month shaping up? We had you work through the spending you’d happily give up in order to purchase your Sticky Note Home—is it working? What have you dialed back? Have you realized that life is quite good with this new home-that’s-only-purchased-on-paper? Or…or… Are things pretty tight? Perhaps, uncomfortably tight?

For all the answers you can get from Google, this exercise of let’s pretend gives you exactly the information you needed. You don’t just wonder if you afford that house—you’ve proved it (one way or the other).

Look at the Whole Picture

These sticky note exercises and games of pretend are all meant to focus you not just on that monthly payment, but to have you step back and look holistically at your finances. When you’re trying to figure how much house you can afford, there will be tradeoffs that the calculators do not mention.

When you buy too much house, you are by definition not buying something else. And that something else could be paying down those pesky student loans, or those last two credit cards. That something else could be funding your retirement. Maybe that something else could be a nice family vacation each year.

Get clear on what you really want first and foremost. Then stress-test that big House Want against all of your other wants, play pretend and live with it for a while, and then make the call. You’ll do great.

Want to turbocharge your savings for a down payment and get crystal clear on how much house you can afford? Make it easier with You Need a Budget—try it free for 34 days.

.jpg)