.svg)

.png)

.avif)

Key Takeaways

Quick Summary: Most emergencies aren’t really emergencies—they’re expenses you can plan for. YNAB can help you replace the vague “emergency fund” with intentional categories that make you feel calm, prepared, and in control.

- The traditional “emergency fund” mindset keeps you stuck worrying about the unknown.

- With YNAB, you plan for life’s surprises by assigning dollars to specific, realistic categories.

- Over time, you won’t need an emergency fund at all, because you’ll already be ready for whatever comes your way.

Money glow-up achieved ✨ Updated November 2025

You’ve probably heard it a hundred times: "You need an emergency fund." But what if the best way to prepare for emergencies is to stop thinking of them as emergencies at all?

What if we could get so good at expecting the unexpected that we stopped experiencing financial “emergencies” altogether? And that big chunk of change sitting in your savings account—what if it was for something much more specific?

A new financial challenge has got me thinking about this a lot lately. Right now, I’m saving up for a new family van. Our current one’s been faithful, but at 20 years old and over 200k miles, it’s becoming more trouble than its worth. So I’m aggressively saving to buy a new-to-me van outright. No debt, no payments. That's just how I roll (literally!).

But here’s the thing: I really want to get this van soon. Every dollar I put into keeping the old one running feels like throwing money away. And as I’ve been saving, I keep glancing over at that other pile of money sitting quietly in my savings account: my emergency fund.

It’s a chunk of change I've barely touched in years. And part of me wonders, why not use it? Why not move it toward the van and get there faster? But the emergency fund feels kind of sacred, you know? Like it’s untouchable. But I move money between categories in YNAB all the time. That’s core to the YNAB method! So I’m sitting there, staring at my emergency fund category, and thinking:

What’s this money actually for?

That question set off a chain reaction that changed how I think about emergencies entirely. I'd rather do emergency funds the YNAB way—with clarity, intention, and knowing exactly what each dollar is supposed to do. Most of all, I want to find a way to never worry about money emergencies again.

.avif)

The Old Emergency Fund Mindset

Traditional financial advice teaches us to build a big, vague cushion of cash. Car breaks down—Emergency fund. Fridge dies—Emergency fund. Surprise medical bill—Emergency fund. It becomes a catch-all for anything that wasn't on your radar.

It’s a well-meaning strategy, rooted in the idea that if you just set aside enough, you’ll be safe. But in practice it often creates a nagging anxiety. What if it’s not enough? You might worry about opportunities you’re passing up by letting that money sit. And when you do need to use it, there’s a subtle guilt that comes with dipping into a pile labeled "emergency."

This mindset makes sense—if you don’t have a better way to plan. But it keeps you stuck in worry mode.

But most emergencies aren’t really emergencies. They’re just expenses you plan for.

And once you learn how to expect them, everything changes.

The YNAB twist

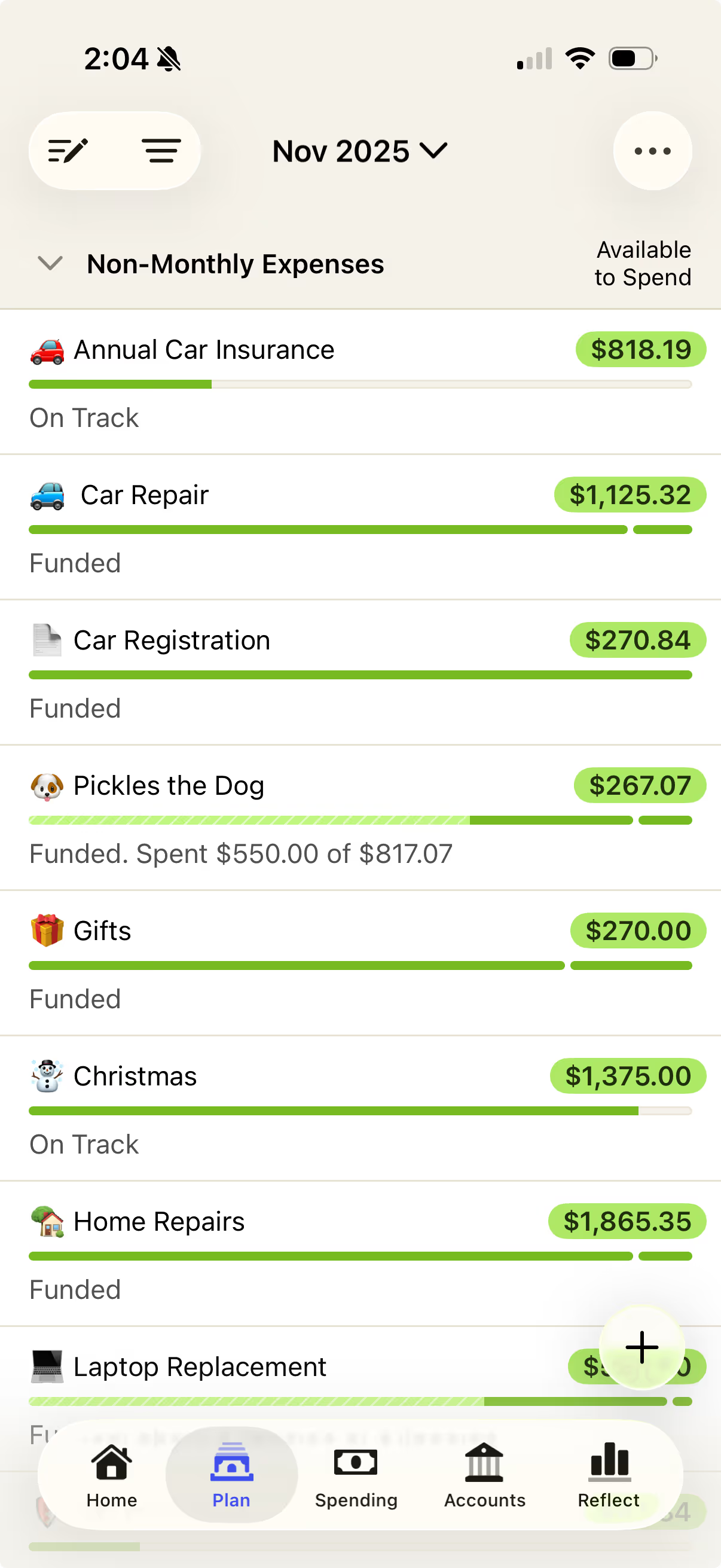

YNAB turns the emergency fund idea on its head. Instead of keeping a lump sum of money off to the side "just in case," you learn to assign every dollar a job. That includes setting aside dollars for non-monthly expenses: car repairs, vet visits, insurance premiums, appliance replacements, and even a job loss fund to cover expenses if you have a disruption in income.

At first, this might feel counterintuitive. Isn’t it safer to have that one big pile of emergency money? But over time, something shifts. You start to see that when you give your dollars specific jobs—like "new tires" or "unexpected dental work"—you don’t just feel more organized. You stop worrying about money. You feel calm, confident, and prepared… because you are!

And when the inevitable happens? You just pay for it. No guilt, no scramble, no drama. Because the money is already there for that specific purpose.

How YNABers Evolve

This is what we see again and again with long-time YNABers. They don’t save money for its own sake. They save for specific jobs—all the unexpected expenses that it turns out you can plan for. And their relationship to "emergencies" transforms in stages.

Stage 1: You still need an emergency fund

When you’re just starting out, you probably haven’t had time to think of every non-monthly expense yet. You’re still getting the hang of the method, and your categories may not be fully built out. So yeah, having a generic emergency fund can help.

And honestly? That’s okay. There are going to be forgotten expenses. Categories that get overwhelmed. Maybe you haven’t had time to build up a cushion yet, and payday still feels like a finish line you’re crawling toward. In that season, an emergency fund can be a life raft. Use it. Lean on it.

But don’t stop there. Because the goal? To make that emergency fund obsolete—and to stop worrying about what’s around the corner.

Stage 2: You need an emergency fund less and less

As you use YNAB, your categories get bigger and you get really good with money. You’ve lived through more "surprises" and built funds to handle them. The fridge died once, and now you’ve got a Home Maintenance category. You forgot about back-to-school shopping last year, but not this year.

You’re a month ahead, your cash flow has improved, and you’ve got dollars sitting in places that make sense. Maybe you haven’t touched your emergency fund in a while. Or maybe you have, but you realized you didn’t actually need to.

You know you have the skills and the cash to handle almost any emergency life can throw your way. But you might still hang onto that emergency fund—just in case.

But something's different now: you don’t rely on it. And that’s a huge shift. The late-night money worries start to fade.

With YNAB, you can have a better emergency fund. This YNAB Template will show you how!

Stage 3: Your Emergency Fund Lives in a Bunch of Different Categories

Eventually, many YNABers reach a point where they haven’t touched their emergency fund in years. That’s when everything clicks.

With emergency fund dollars stashed in categories for expenses that will inevitably come up, you’re not living on the edge anymore. You’ve proven to yourself, over and over, that you can handle life’s curveballs. You’re still human. Things still happen. But now when they do, you don’t flinch. You look at your categories, move some money around, and move on—without worry.

This shift isn’t just theoretical. It’s a milestone YNABers celebrate. I talked about this briefly on a Budget Nerds episode, and after reading the comments, I knew I had to think and write about this more!

SPOT ON. I'd love to be in a position where my emergency fund could be updated to a job loss fund. That is a great way to look at things.

We've reached this level of flexibility to use that money for things that might come up and still be fine, while also weighing the trade-offs. I really hope you write a blog about this!

So Do You Need an Emergency Fund?

If you're new to YNAB, the answer might be yes—for now. It’s a useful tool. A helpful starting point. But if you stick with it, if you practice the method and let your categories evolve, something remarkable happens.

That emergency fund becomes quiet. Then it becomes optional. Then it becomes scattered across your YNAB plan with dollars employed for very specific jobs.

When you stop waiting for the other shoe to drop, and start planning for real life instead, you’ll find something even better than a pile of emergency cash. You’ll stop worrying about money. For good.

Ready to ditch the vague emergency fund and start planning instead? Start your free 34-day YNAB trial today.

FAQ

Q1: Should I still have an emergency fund if I’m new to YNAB?

A: Yes—for now. When you’re just getting started, an emergency fund acts as a helpful safety net while you learn the method and build out your categories.

Q2: What replaces the emergency fund in YNAB?

A: Instead of one big “just in case” pile, YNABers spread those dollars across targeted categories like car repairs, medical costs, or job loss. Each dollar has a clear purpose.

Q3: What if something truly unexpected happens?

A: You can still move money between categories as needed. The difference is that you’ll be calm and prepared because your money is already organized and flexible.

Q4: How do I know when I can stop keeping a separate emergency fund?

A: When you consistently handle surprise expenses with existing categories and rarely dip into your emergency fund, you’ve reached the point where it’s no longer essential.

.png)

.jpg)

.png)