.svg)

.png)

Are Your Budget Categories Earning Their Keep?

.avif)

I have to imagine that, when YNABers meet in the wild, after the initial jubilant shrieking and chest-bumping, they collect themselves for a few moments to talk shop budgeting. (I mean, that’s basically how Team YNAB behaves on the first day of our annual retreat, plus or minus a hug-a-thon and several board games.)

And, in that conversation, I’d be willing to bet a free month of YNAB to new users that they ask the question that’s been burning on budgeters’ lips since the dawn of YNAB: How many categories do you have in your budget?

Now, let’s say that you and I bumped into one another, and we had just such a conversation. I could give you the answer. I have 41 categories in my budget. But, being a teacher at YNAB, I’d have let you down. 41 categories might not be the right number for you. In fact, my number is irrelevant.

What you really need to know is how to figure out your number. So let’s take a look…

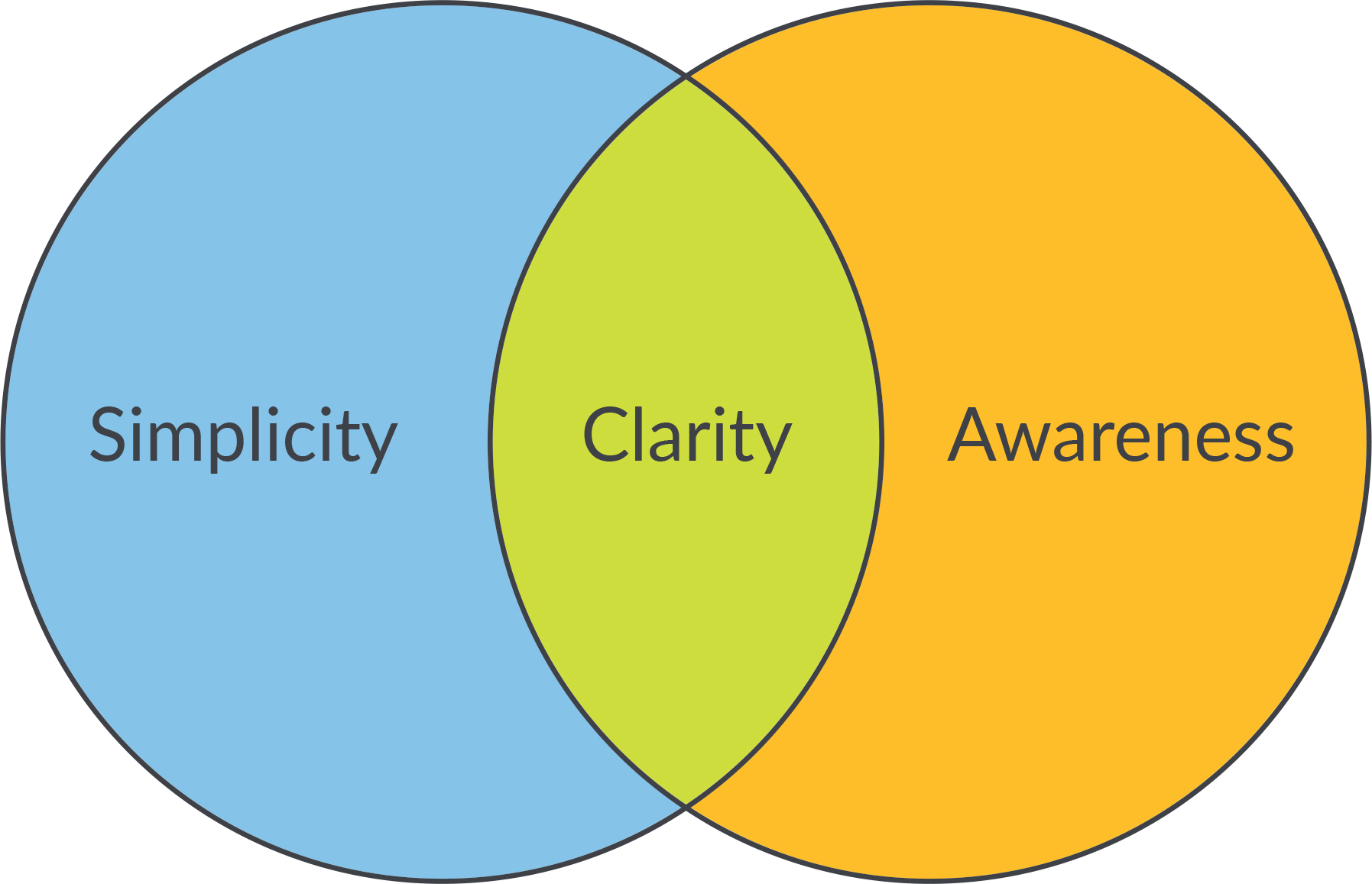

Venn Is the Magic Number

There are two considerations that will help you decipher the precise number of categories that you need:

- Simplicity – The motor oil of your budget, simplicity is a critical component that keeps things running smoothly and easily so that you keep budgeting. Never underestimate the benefits of a simplified budget.

- Awareness – Sticking with our car analogy, awareness is like your windows and mirrors, allowing you to see current conditions from every angle—important if you want to stay on the road, maneuver around obstacles and get where you’re going.

Slap simplicity and awareness into a Venn diagram and, in their intersection, you’ll find clarity … category clarity, that is.

Clarity Is a Balancing Act

Clarity, for our purposes, is the minimum number of categories that you need for awareness and the maximum number that you can have before you’ve breached simplicity.

In other words, too few categories, and you lose awareness (which is necessary to inspire behavior changes so that you can reach your financial goals). Too many categories, and you’ve lost simplicity (which keeps you in the game).

Let’s use an example to make this “clarity” thing, uh, clear …

The Importance of Simplicity

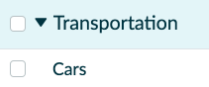

Imagine that the ‘Transportation’ category of your budget looked like this:

That’s 14 categories. We have oodles (and oodles) of awareness, but we’ve lost simplicity.

Look closely. How useful do you think it’ll be to have a category for wiper fluid for your Ford? You’ll spend extra time categorizing your transactions, and for what? There’s very little value in separating your wiper fluid expenditures by vehicle, or even at all. It would make more sense to lump those purchases into a catchall maintenance category.

Plus, with so many transportation categories, you’ve sacrificed clarity! The whole point of budgeting is having the information that you need in order to improve your finances. Do these 14 categories help you do that? Think about it:

- Will you spend less money on wiper fluid because you’ve made a category especially for it? Nope. If you need wiper fluid, you just buy it.

- Will you spend less money on oil changes and repairs? Nope (though you can postpone them in a pinch).

- Will you spend less money on car payments and insurance? Again, nope!

The only category that you might be able to affect with behavior change is gas, and that depends on your transportation needs.

The Importance of Awareness

On the other hand, too much simplicity isn’t helpful, either. Imagine, instead, if your budget looked like this:

It sure is simple, but you’ll have no idea what kind of car-related expenses you’ve paid for! Without awareness of where the cash went, again, we’ve lost clarity. This budget won’t help with critical decisions like:

- Is one of my cars costing a lot in repairs, lately? Is it maybe time to replace it?

- How much am I spending on gas?

- Should I consider changing my insurance coverage to lower the premium?

Arriving at Clarity

Let’s say that your Ford is nine years old, with heavy mileage, and the Mazda is three. Knowing how much the Ford is costing in repairs is useful information that can help you decide when to say goodbye and find a new car.

So, you might arrange your categories like this:

With five categories, now we’ve got both awareness and simplicity.

And there’s a middle ground here, as well. You could track each car in a different group. Dave, one of YNAB’s teachers, does this. He wants to know the total cost of each car. I get that. Here’s what it looks like:

We’re up to eight categories, but it still feels simple. We get a little more information, and possibly an increased feeling of clarity. Of course, clarity isn’t just about the number of categories …

Categories Find a Way

Before adding a new category to your budget, a good litmus test is to ask yourself, “What will I do with the information I gain from adding this category? Will it help me change something?”

If the answer is no, you probably don’t need it. If you’re not sure, leave it out! If you’re wrong, you’ll know because you’ll feel yourself reaching for it. You’ll struggle when you categorize transactions wondering, “Where should I put this?”

In a way, you’re forcing the category to earn its spot in the budget. And, from the perspective of habit-building, adding a needed category is easier than removing an unneeded one because if you train yourself to use a category, you will.

So, start with fewer categories that really deserve to be in your budget. If you’re missing any, they’ll find their way in.

The Dunkin Donuts Clause

In our quest for simplicity, are we never allowed to break down our categories to our most granular spending decisions? Absolutely not! In fact, a little over seven years ago, for a little while, I had a category in my budget for Dunkin Donuts. That might sound crazy—Dunkin Donuts is a payee not a category! I know, I know. But, here’s the thing …

At the time, my commute was more than an hour long, one way. I was insanely busy, and I was in the car for two and a half hours a day. I was perpetually exhausted. To make it all bearable, I’d reward myself on the drive home with a hazelnut Coolatta (and sometimes, maybe/perhaps/probably a donut … or two).

Initially, I categorized my treat under ‘Eating Out’ and my eating out category exploded. When I drilled down into the data, I saw all the purchases. Yikes! I didn’t even realize it was happening. I’d lost awareness, and I definitely didn’t want to spend that much at Dunkin Donuts.

To dial things in, for a while (not forever), I added a category for Dunkin Donuts and budgeted specifically for those purchases. I wasn’t ready to quit the drive-through, completely, but I did cut way back. Once I had my habit under control, I hid the category and went back to using my eating out category.

The awareness that I gained by using my Dunkin Donuts category led to change—totally worth the extra budgeting effort. And, now, I hardly ever go there!

Go Forth, and Find Your Category Number!

In conclusion, when adding categories, let these questions guide you:

- Will the category give me greater awareness without creating unnecessary tedious work?

- Will this category help me change my spending behavior?

And always, always, always start with fewer categories and let them earn their way in.

For more help customizing your budget categories, drop into one of our free, online classes. They’re only 20 minutes long, and we’re here to help you with all of your questions!