.svg)

.png)

.png)

.svg)

Is Your Paycheck Running Your Life? Here's How to Tell

.avif)

Key Takeaways

Quick Summary: Ever felt like you can’t make a decision until you get paid? That’s your paycheck running your life. Here’s how to take back the reins and finally breathe easier around money.

- Getting one month ahead of your bills flips the script from reacting to planning with confidence.

- Saving one month of money (just once!) breaks the paycheck-to-paycheck cycle for good.

- When timing works for you instead of against you, life gets emotionally, logistically, and mentally easier.

If you’ve ever worried about money—really worried, the kind that hums like the small world song stuck in your head for years—you’re not imagining the pressure. That worry is real, relentless, and quietly exhausting… and you shouldn’t have to carry it alone.

There's a secret way out of this worry, one I've shared with YNABers for years, and you can learn it too.

This kind of worry isn’t a personal flaw. It’s a skill gap. It’s the predictable outcome of living reactively, always waiting for the next payday to unlock the next part of your life. You’re doing everything you can, yet still feel behind—because your paycheck cycle keeps you behind.

The reason why it feels so impossible to get good with money is because you’re trying to make decisions inside a timing trap. When your bills arrive before your money does, even simple choices start to feel heavy. And that’s the part no one talks about: the timing, not the amount, is what’s running the show.

If you’re living paycheck to paycheck, your life runs on your employer’s pay schedule.

But what if you could break free from that cycle? How much easier would it be to get better with money? How much less money worry would you feel?

With some focus and some new skills, it is possible. Let me show you how.

.png)

When your money comes in pieces, you have to plan in pieces.

First, let me make the problem super clear. Every financial decision you make is dictated by when someone else decides to pay you. Here’s what that might mean, practically:

- It means the bills are piling up on the kitchen table. You want to pay them, but you’re waiting to get paid.

- It means saying no to lunch with a friend because the lunch date is before payday.

- It means telling your kid they can’t go on the field trip—not because you don’t have the money, but because you don’t have the money yet.

- It means you have to go grocery shopping on Friday night with everyone else who just got paid, because you won’t have the money until then.

When you live this way, it affects more than money. It drains your energy.

You’re constantly thinking about it, checking it, adjusting it. The timing of your paycheck creeps into everything. You’re forced to manage the mind-consuming minutiae of money.

And it’s not only emotionally draining, it keeps you perpetually behind. (I know, I've been there thinking money stress was just baked into being an adult!)

Assigning money to your plan becomes fragmented, time-consuming, and never-ending—because you’re always reacting to what just came in instead of planning for what’s ahead.

And the more often you get paid, the more often you have to think about it.

Let’s take someone who’s paid weekly and their spouse is paid twice a month. They’re not just managing money—they're managing it six separate times.

Six times to sit down and figure out which bills to pay, six times to worry whether it’s enough, six times to basically re-decide the same things. Every. Single. Month. The more paychecks you get, the more fragmented your life feels.

Each new paycheck restarts the mental cycle of money worry: spend, track, regret.

It’s inefficient. It’s exhausting. You’re managing your life in tiny pieces, paycheck by paycheck, instead of seeing the whole picture.

.png)

You feel like you’re bad with money because of a timing problem.

Living this way day after day leaves you feeling like you’re bad at money. And you may be! But it’s not because you’re a bad person. It’s because you’ve got a timing problem.

Right now, you’re timing behind your bills. The bills get there first in the race we call daily life. And you? You’re sitting around waiting for that almighty paycheck. What you need to do is flip that timing.

Imagine this: Instead of staring at a big pile of bills and waiting for the money to pay them, you’ve got a big pile of money and you’re just waiting for the bills to roll in.

It can happen. We can’t always change the timing of payday, but we can get ahead of it. You’ll still be timing your cash flow—you’ll just be timing really well because you’re planning ahead of your bills instead of reacting to them by giving every dollar a job.

You’ve just done the impossible. You changed your paycheck schedule to monthly without even having to speak to your boss.

Once you solve this timing problem, when you get paid doesn’t matter anymore. You can pay bills calmly, confidently, on your schedule—not your employer’s.

You no longer have a timing problem, and suddenly life gets easier.

Life gets easier emotionally.

You no longer wake up with that low-grade hum of money anxiety. Instead of reacting to each new expense with a knot in your stomach, you can breathe easy knowing you’ve already prepared for it.

Life gets easier administratively.

Paying bills or planning spending stops feeling like an endless game of catch-up. You sit down once, see the full picture, and make clear decisions. No more juggling due dates or second-guessing what’s left.

Life gets easier logistically.

The chaos of timing disappears. You pay things when it makes sense for you, not when your pay cycle dictates. Heck—put your bill on autopay confidently! You know the money will be there. This frees your time, energy and attention for the rest of your life.

How to break the timing problem

There are two pieces to getting past this timing issue forever:

- Getting there.

- Staying there.

They are distinctly different. Getting there is the hard part. Staying there is so easy you won’t even believe it’s real.

Getting there

To get there, you need to save up one month’s worth of spending. Now we have to do a little math, but fear not—YNAB will help you!

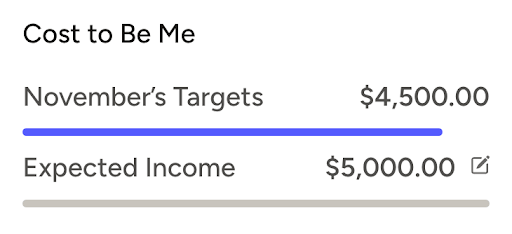

Just look at your Cost to Be Me:

In this example, I’m bringing in $5,000 and have targets set to spend or save $4,500. That gives me a monthly margin of $500.

So what does this tell us?

- I have $500 that I can put towards making the flip and getting ahead of my bills.

- I need $4,500 monthly for spending.

- $4,500 divided by $500 is 9.

That means if I can just put $500 a month aside for 9 months, I’ll save $4,500 and will have enough money to cover an entire month.

Here’s the most game-changing part of this habit change: I only need to do this one time. Hang with me, because this will blow your mind.

Staying there

Let’s say each month I faithfully put my $500 aside for next month. One month—let’s say November—I wake up on the 1st and I have $4,500 to cover the entire month. Now when I’m paid in November, I won’t need that money for November. I can set that money aside for December!

- Paycheck #1 arrives on November 10th: $2,250. I don’t need it for November, off it goes to December.

- Paycheck #2 arrives on November 24th: $2,250. Again, I don’t need it for November, off it goes to December.

On December 1st, I wake up and boom—December is covered. Instead of taking nine months this time, it only took one. My paychecks can now replenish what took me nine months to save in just a month!

Do you see? This problem of timing paychecks to bills is not about how much money you have. It's about when you have the money. It's all about timing.

You are now perpetually ahead of your spending. Getting there took nine months, but staying there is drop dead simple. You just set the money aside for next month when you’re paid.

.png)

The key benefit of breaking the paycheck to paycheck cycle

When you solve the timing problem you have TIME to respond to problems. If you lose your job, you aren’t immediately in a crisis, you have time to figure out what to do.

When you’re not living paycheck to paycheck, it doesn’t matter when you get paid. But when you are living paycheck to paycheck, when you get paid is the only thing that matters.

You’re now free to move on to higher-level thoughts. You can put your bills on autopay, confident that the money will be there. Shop for groceries any day you please—just check that grocery category on your way into the store.

The quality of your decisions improves when you’re fully funded on the first. You can be good with money. And I promise you this: your priorities will emerge much more easily when you can see the whole picture and assign your money all at once, not just tiny pieces of it dripped out over the course of the month.

Shifting your timing changes everything.

When your life runs on your employer’s pay schedule, you’re constantly reacting—always one step behind your bills, your plans, and your peace of mind. But shifting your timing changes everything. Getting fully funded on the first and ahead of those bills isn’t just about money; it’s about making everything easier.

It’s how you stop surviving by the paycheck and start living by your plan.

Have you ever worried about money? You’re not alone. Download YNAB, get good with money, and never worry about money again.

FAQs

Q1: Why does paycheck timing create so much stress?

A: Because you’re reacting instead of planning. When bills arrive before the money does, every decision becomes an emotional one.

Q2: Will getting ahead help me stop worrying about money?

A: Yes. When you’re fully funded on the first, you stop second-guessing and start trusting your plan.

Q3: How can YNAB help me get ahead?

A: YNAB helps you get ahead by showing exactly what your money needs to do next and helping you build enough margin to cover a full month at once. When you assign every dollar a job, you stop reacting to each paycheck and start planning with confidence.

Q4: What if my income is irregular?

A: The timing principle still works. In fact, you need it more than anyone. Saving one (or more) months worth of expenses will provide badly-needed stability even when paychecks vary.

Q5: Is this approach realistic for me?

A: Absolutely. YNABers with all income levels—from hourly workers to freelancers—have reached one month ahead and felt the shift. Do the YNAB free trial and see for yourself how good it feels to get good with money.

.avif)

.avif)