.png)

.webp)

Imagine waking up every day knowing exactly how your money is paving the way toward the future you want. With YNAB targets, you can pinpoint how much you need each month for all the things that matter to you—from your childcare expenses to your dream vacation.

Targets are at the heart of many successful YNAB spending plans. By setting predetermined amounts for each category, you not only track your progress toward financial goals but also gain a clear view of your monthly financial needs. YNAB simplifies this journey by turning your targets into actionable monthly goals, ensuring every dollar is aligned with your priorities.

Once you start using targets, it’s hard to YNAB without them!

And with the latest update to targets in May 2024, they’re easier to use than ever before. Being the savvy YNABer you are, you’ll likely have no trouble setting targets based on the helpful process right there in your mobile or web app. Just in case, let’s dive into the simple four-step process to set up a target in your YNAB spending plan.

Step 1: Choose a cadence

Bills, expenses, and savings goals come in all shapes and sizes. That's why YNAB flexes with you, adapting to the unique tempo of your life. Targets allow you to set up weekly, monthly, or yearly cadences. For everything else, there’s the custom cadence option, which we’ll go over in another section. Let’s go over those most common options and the kinds of expenses you’ll use them for.

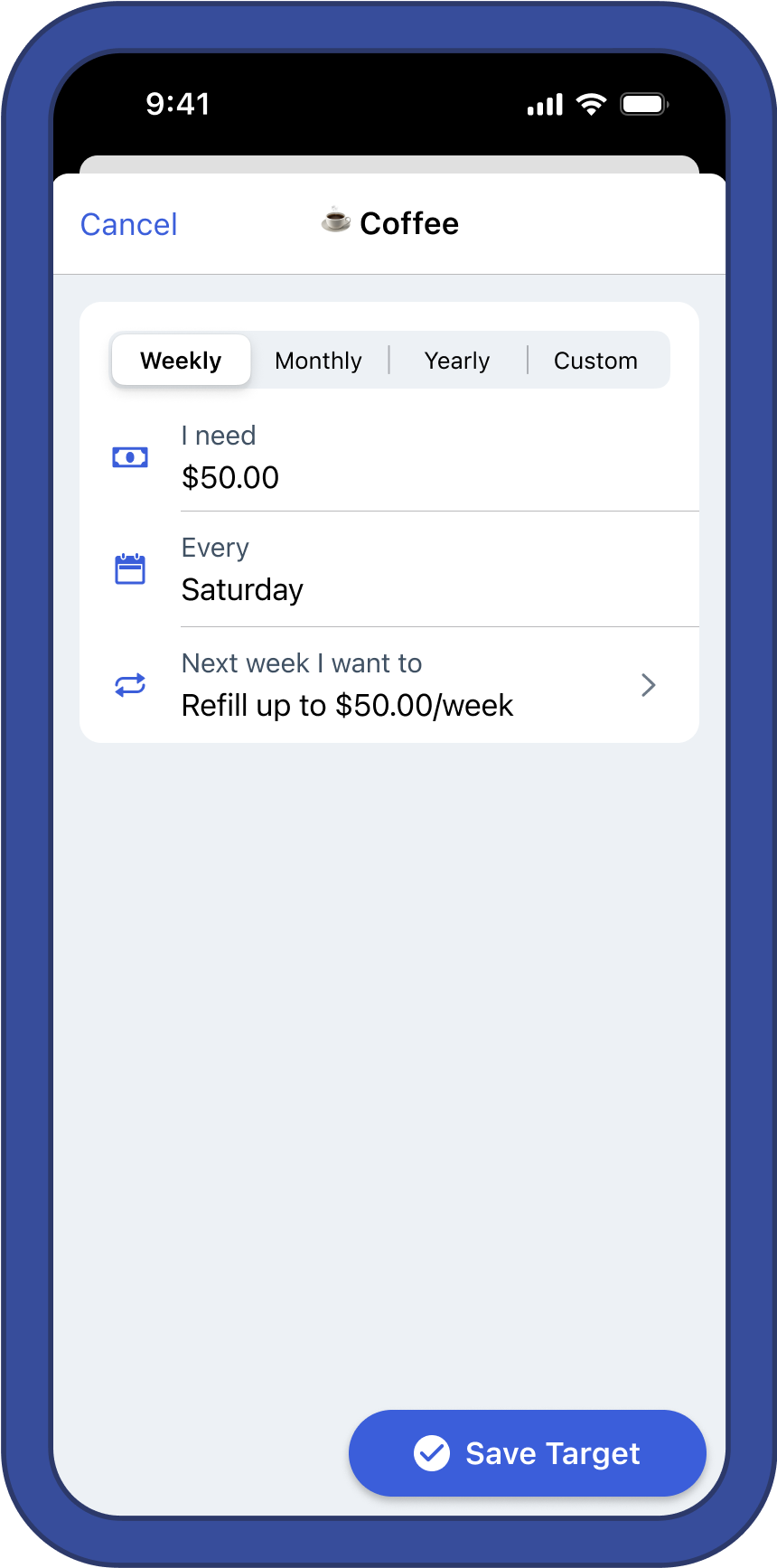

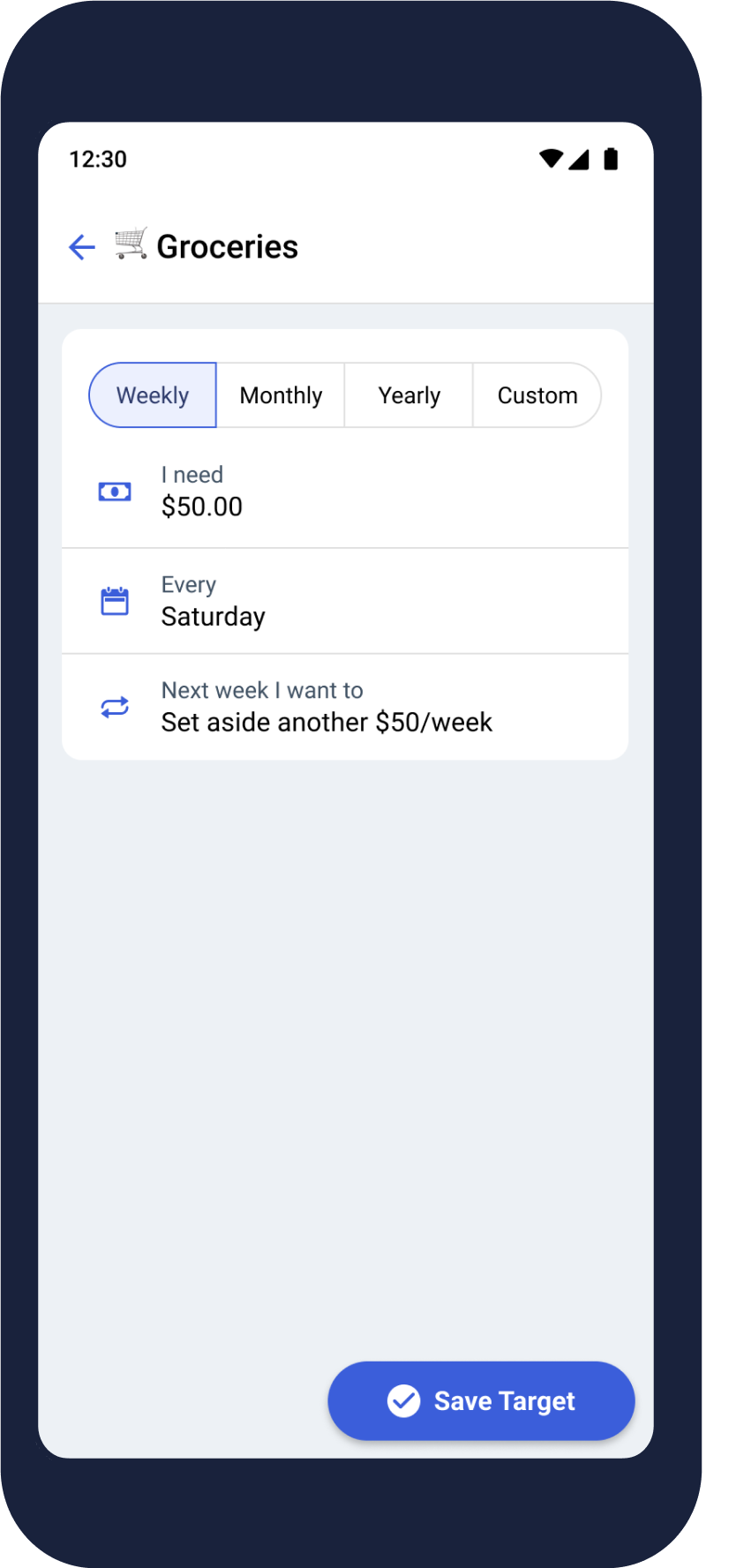

Weekly

Weekly targets are designed for any bills or expenses that you typically spend money on once a week. It’s perfect for that once-a-week childcare bill, your routine trip to the grocery store, or your weekly date night.

What’s nice about weekly targets is YNAB will prompt you to assign a different amount based on the length of the month. So if you pay for childcare every Friday, YNAB will remind you when those pesky five-Friday months come along so you always have enough.

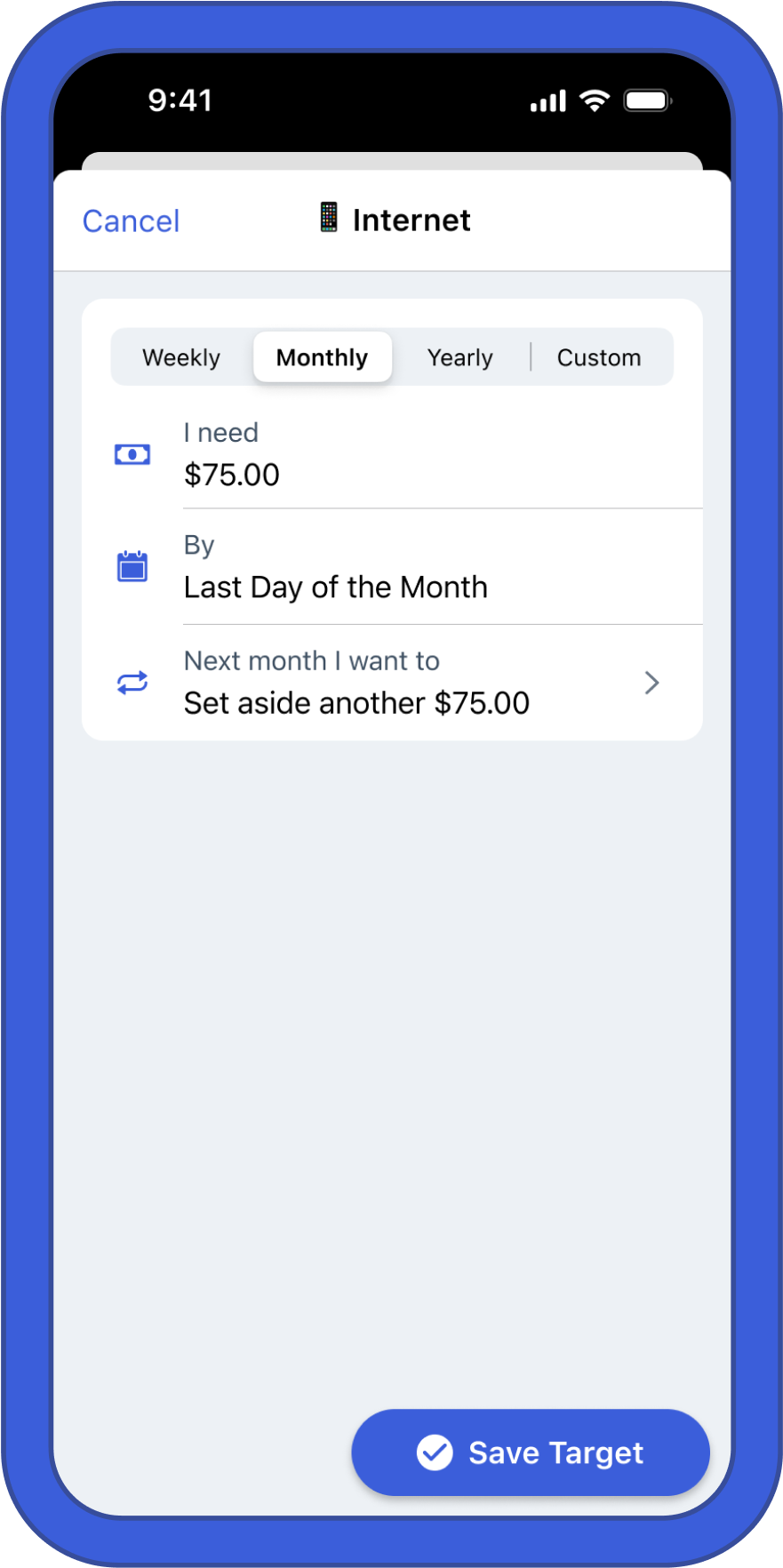

Monthly

Monthly targets are likely to be the most common in your plan. If you want to set aside a certain amount every month, this is the target cadence for you. It works for categories that you spend from only once a month (like rent or your monthly phone bill), but also for categories with variable spending patterns (like your personal fun money).

You can even use it for unpredictable non-monthly expenses that you want to set money aside for every month, like car repairs. Use this whenever you want to save or spend a certain amount in a category every month.

Yearly

Yearly targets are for all your predictable yearly bills and expenses. Think Amazon Prime payment, your property tax bill, even your yearly YNAB subscription! If you have a bill that you pay once a year like clockwork, the yearly target will prompt you to save enough every month to be ready for it. No more scrambling to cover those big yearly bills!

Step 2: Choose an amount

Under the target cadence options, you’ll see a few more fields to describe your expenses in more detail. First you’ll see the phrase “I need…” with a box for you to enter in a number.

Naturally, every target needs an amount. How much money do you need within the time frame of the cadence you chose in step 1? Write it down then stop worrying about the math. YNAB will take it from there!

Step 3: Choose a due date

Next, choose a date that you need the money by. This field will look different depending on the cadence you chose in step 1.

For weekly targets, you’ll see the word “Every” and a drop down box with the days of the week. What day of the week do you typically spend money in that category? If you like to go grocery shopping on Mondays, choose that day, and YNAB will give you a monthly target amount that changes depending on how many Mondays there are in the month.

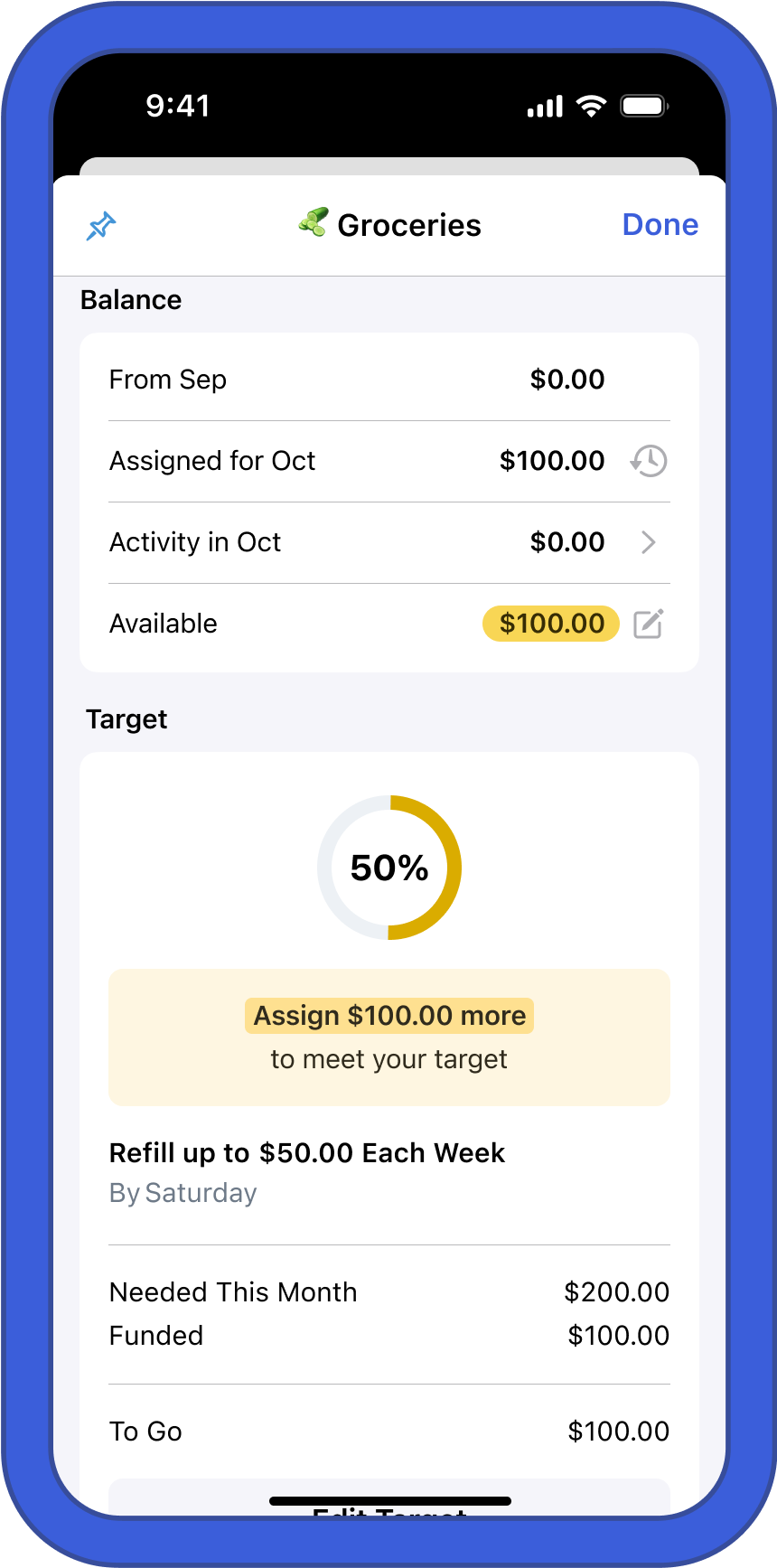

For monthly targets, you’ll see the word “By” and a drop down box with the days of the month. If you have a bill that you always pay on a certain day of the month, choose that date. If it’s a savings goal or a more variable expense, choose “Last day of the month.” This is helpful for notation purposes.

With progress bars on, you’ll see the date that the bill is due listed right next to the category name. But the date you choose on monthly targets also affects how the Underfunded Auto-Assign button auto-prioritizes your categories.

For yearly targets, you’ll also see the word “By” and a date picker where you can choose the year, month, and date of your yearly expense. This date will affect how much money YNAB prompts you to save for yearly expenses every month.

Step 4: Choose a behavior

The last step is to tell YNAB how you want the target to behave once the month rolls over or (in the case of yearly targets) the new yearly cadence starts. For weekly, monthly, and yearly targets, you’ll have two options:

First, you can set aside another full target amount when it's time to fund the target again. This is the simplest and most common option. For weekly and monthly targets, you’ll continue funding the same amount regardless of how much money rolled over from the previous month or year. Use this for regular bills, subscriptions, or for when you want to save up money in your category over time.

Second, you can refill up to the full target amount when it's time to fund the target again. This is commonly called the “top-up” option. This will set the target to have your target amount on hand each month or year. Anything you don’t spend will be applied to next month’s or year’s target.

Use this for categories where you want to spend a certain amount every month or year but don’t want to save money over time. Gasoline, fun money, or dining out are common examples.

Custom targets—more options

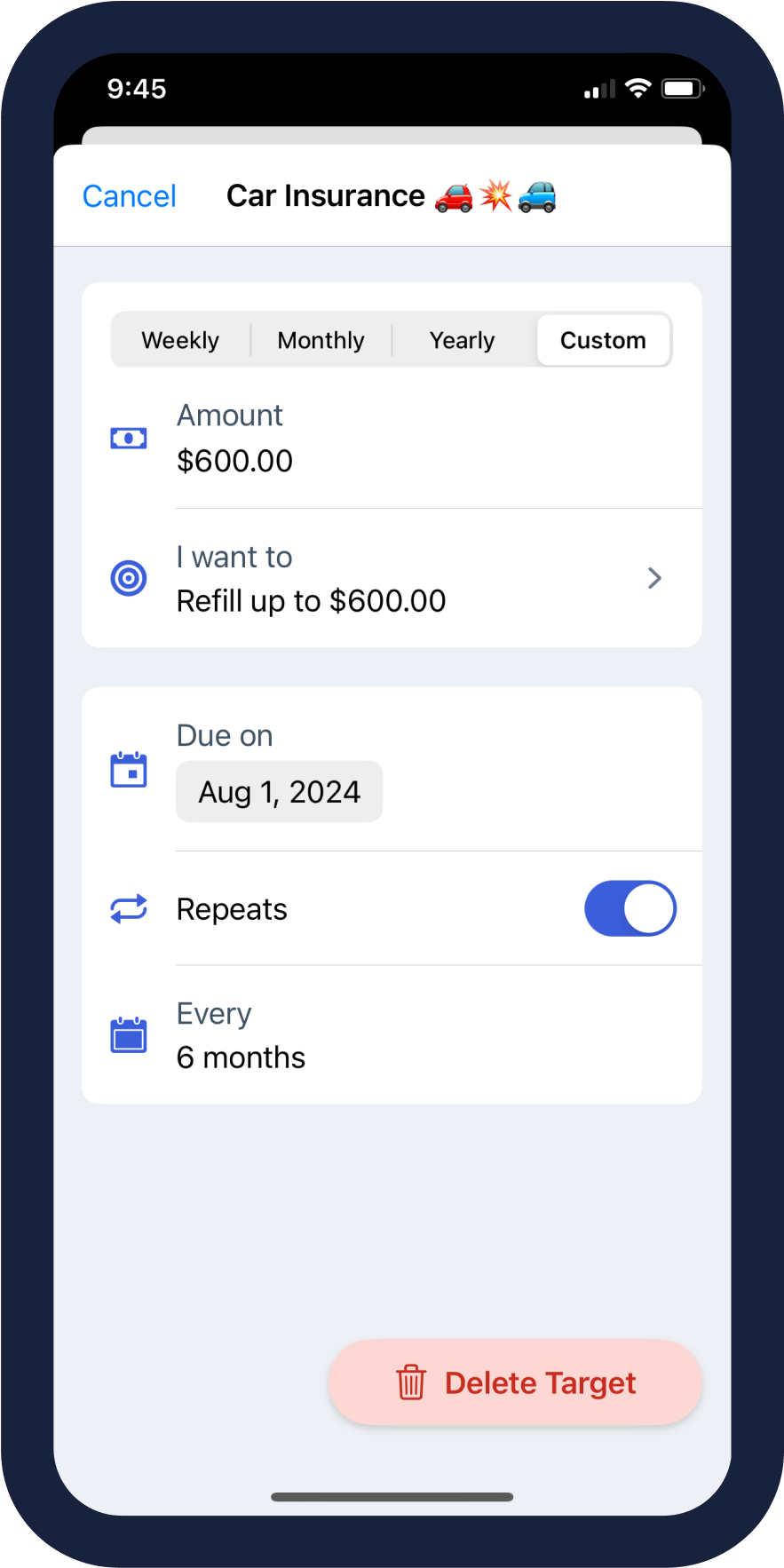

If you’re a more seasoned YNABer, a true optimizer, or you just want to have more target options, the Custom cadence is for you! You’ll still set an amount like the other options, but the cadence is more flexible. Choose an appropriate due date, then if the expense repeats, toggle on the “repeat” option and choose a custom cadence. You can set it to repeat every 1-11 months or every 1-2 years.

Some categories don’t need a repeating target, because they’re a one-off savings goal like a home down payment or a new Onewheel (I still haven’t broken my collarbone, knock on wood). For these kinds of expenses, you’ll have a special behavior that’s only available for custom targets.

The “Have a Balance of…” behavior will set the target to make sure you have a certain balance in the category by a certain date. If you spend from this category along the way, YNAB will prompt you to assign more in future months to play catch up.

You can also choose the “Have a Balance of…” behavior on custom targets without setting a date. YNAB won’t prompt you to set aside a certain amount every month, but it will track your progress toward your savings goal.

Credit card and debt payment targets

YNAB also has targets on categories that are specially paired to an account. Specifically, there are two options for targets on credit card payment categories and Debt Payment Targets for categories paired with a loan account.

Credit card payoff targets

Credit Card Payment targets are specifically for the credit card payment category that YNAB automatically creates when you add a credit card account. They are designed to help you pay off debt on your card from previous months. There are two options:

The Pay Off Balance by Date target lets you choose a date you want to have the card paid off by. YNAB will calculate how much you need to set aside in the payment category based on the date and your credit card balance.

The Pay Specific Amount Monthly target lets you simply enter an amount that you want to set aside every month to pay off past debt on the card. YNAB will always prompt you to set aside that amount no matter what.

Debt payment target

At face value, the Debt Payment target works exactly like a monthly target. You set the monthly amount and the date and YNAB will remind you to assign that amount every month.

Debt payment targets automatically use the “set aside another full target amount” behavior, which means you’ll be prompted to set aside the full target amount regardless of how much money rolled over from the previous month.

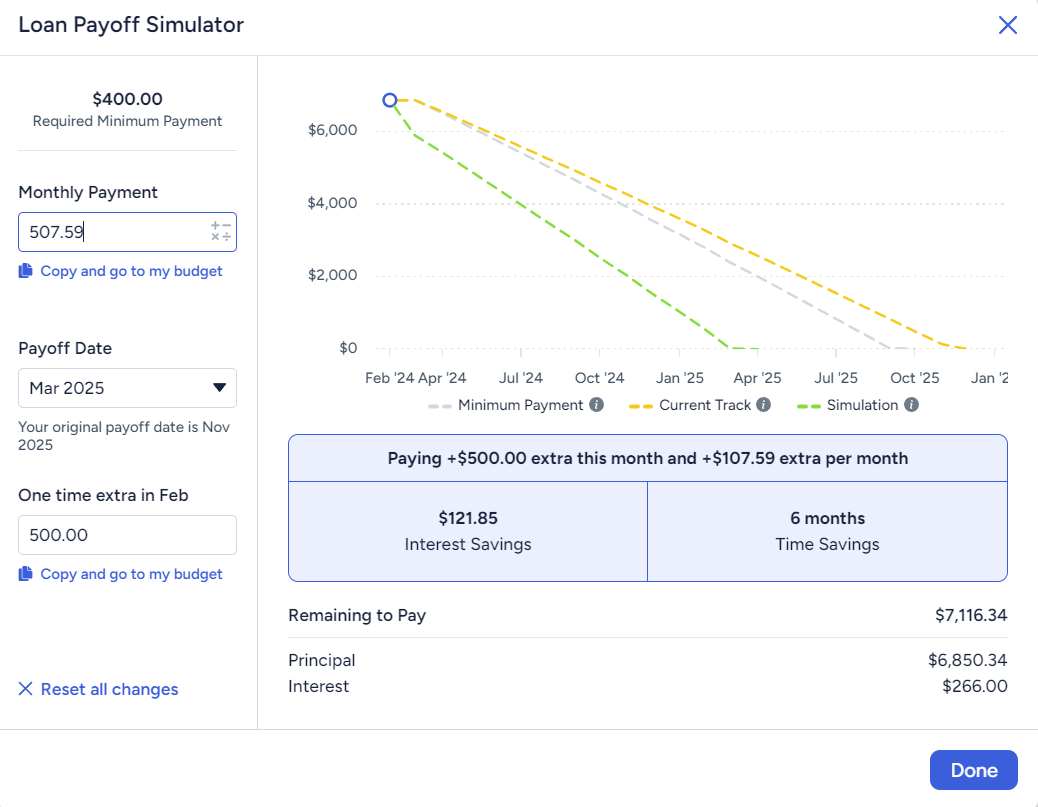

But the awesome thing about Monthly Debt Payment targets is they are specially paired to a loan account, which includes extra data visualization features and the Payoff Simulator, a sandbox that will let you dream a little without changing anything in your plan. If I make a one-time extra mortgage payment, how much interest will I save over 15 years? If I pay $100 extra every month on my car loan, how much faster will I be able to pay it off? The Payoff Simulator can answer these questions!

A simplified version of the Payoff Simulator is also available in the budget screen right where you set your target.

In order to use a debt payment target, you’ll first need to set up a loan account to pair with the category. If you’d rather not use a debt payment target, you can use a monthly target instead. But even if you’re not ready to pay extra on your loans, it’s a good idea to go ahead and use this target for your debt payment categories so you can easily unlock these tools in the future.

Snooze a target

We use targets to remind us how much we need in a category in a typical month. But not all months are typical. That’s what the Snooze a Target feature is for! If, for any reason, you don’t want to fully fund a target this month, you can snooze it to remove the yellow underfunded alert until a new month begins. This allows you to pause a target without removing it completely.

We see people use this most commonly in the middle of the month. If you move money out of a category to cover overspending or fund a higher priority, the category’s available amount will turn yellow to warn you that it is underfunded. Even if you fully funded the target at the beginning of the month, you’ll still get that warning when you make a change, so the Snooze feature is perfect when that happens.

Other times, you just can’t fully fund a target this month, either because your income was lower than expected or because a higher priority took preference. Snooze that target so you don’t get the constant underfunded alert, and you’ll get a reminder to try again next month. If you consistently can’t fund a target, it might be a sign that the category is not a priority or the amount is unrealistic. In that case, consider changing the target more permanently.

With YNAB’s targets, you can capture and slay every bill and expense while making those financial dreams come true.

Cheers and happy YNABing!

Want to stay in the know about the latest product updates and best money stories around? Sign up for our YNAB newsletters—they're short, informative, and occasionally hilarious.